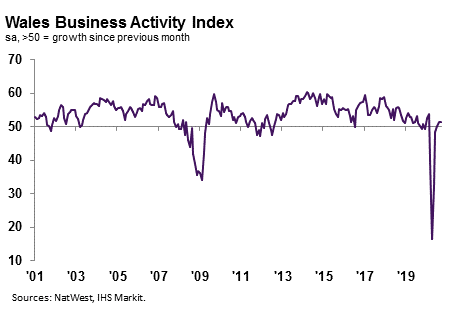

The headline NatWest Wales Business Activity Index – a seasonally adjusted index that measures the month-on-month change in the combined output of the region’s manufacturing and service sectors – registered 51.3 in September, down slightly from 51.5 in August. The latest data indicated only a marginal expansion in Welsh private sector business activity. Although a number of firms linked the rise to greater client demand, others noted that new order inflows remained historically subdued.

Welsh firms signalled a slower upturn in new orders during September, albeit still solid overall. Growth in new business was commonly linked to the reopening of client businesses following extended lockdown measures. The softer expansion was the second-strongest since July 2019 and reflected the UK-wide trend.

September data signalled further optimism among Welsh private sector firms regarding the outlook for output over the coming year. That said, the degree of confidence slipped to the weakest since March, as some firms expressed greater hesitancy amid the ongoing pandemic and global economic downturn. The level of positive sentiment was much lower than the UK average.

September data signalled a further marked contraction in workforce numbers across the Welsh private sector. Firms stated that the drop in staffing numbers was due to redundancies and efforts to cut costs amid weak sales. The rate of job cuts eased to the slowest for six months, however, reflecting the trend seen across the UK as a whole.

Welsh private sector firms recorded a slight decrease in backlogs of work at the end of the third quarter, with the rate of decline quickening marginally. Companies often cited sufficient capacity as a key factor behind the depletion of outstanding business. The rate of contraction was much slower than those seen during the depths of the pandemic, however.

Welsh firms registered a fifth successive monthly increase in cost burdens during September. The increase was strong overall, but eased to the slowest since June. Although some noted that higher input prices were linked to greater supplier charges, others stated that redundancies had reduced pressure on costs. Nonetheless, the rate of inflation was faster than the UK average.

Average selling prices continued to increase at a solid pace at the end of the third quarter. Panellists linked higher charges to the partial pass-through of greater costs to clients. The rate of inflation matched that seen in August and was the fastest of the 12 monitored UK areas. The increase in charges seen in Wales contrasted notably with the slight decline seen across the UK as a whole.

Kevin Morgan, NatWest Wales Regional Board, commented:

“Following a modest pick-up in August, the Welsh private sector signalled a moderation in activity growth at the end of the third quarter. Nonetheless, the further expansion indicated a marked turnaround from the substantial decline seen in April.

“In an effort to reduce cost burdens, firms cut back on employment through further redundancies. Staffing fell at the slowest pace for six months, but pressure on capacity remained weak. Impetus to hire may not return any time soon, as business confidence dwindled once again to its lowest since March.

“Encouragingly, selling prices continued to rise solidly, contrasting notably with the marginal fall seen across the UK as a whole.”